Every financial market operates within a structure that includes costs. These costs are not incidental. They are embedded in how markets function and how trading infrastructure is maintained. For traders, understanding these costs is not a secondary detail but a fundamental part of responsible participation.

While price movement receives most of the attention in trading discussions, the mechanics of trading costs often receive less scrutiny. Yet spreads, financing charges, and commissions directly influence trade execution, position management, and long term account sustainability. A clear understanding of how these costs arise and how they affect different types of trading activity helps create more realistic expectations and supports better planning.

This article examines the primary forms of trading costs commonly encountered in leveraged and multi asset trading environments. Rather than focusing on comparison or optimization, the goal is to explain structure. When traders understand how costs work, they are better positioned to interpret their impact within the broader context of market participation.

The Spread as the Core Transaction Cost

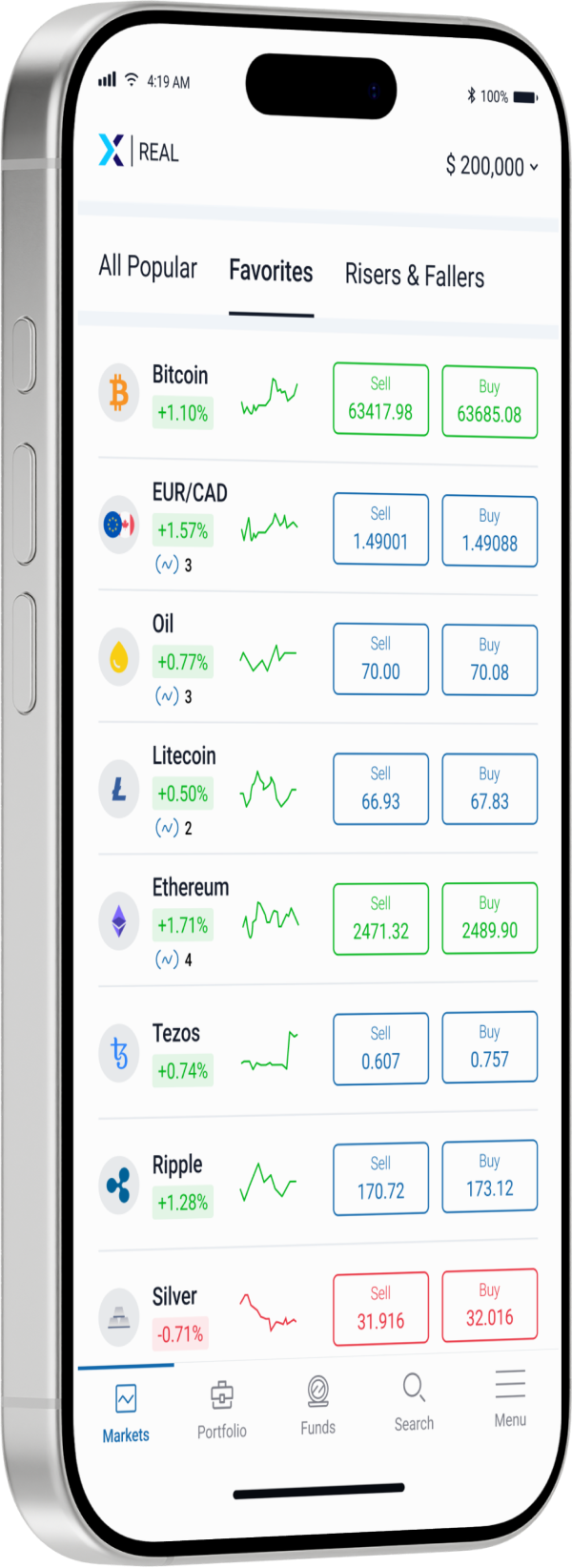

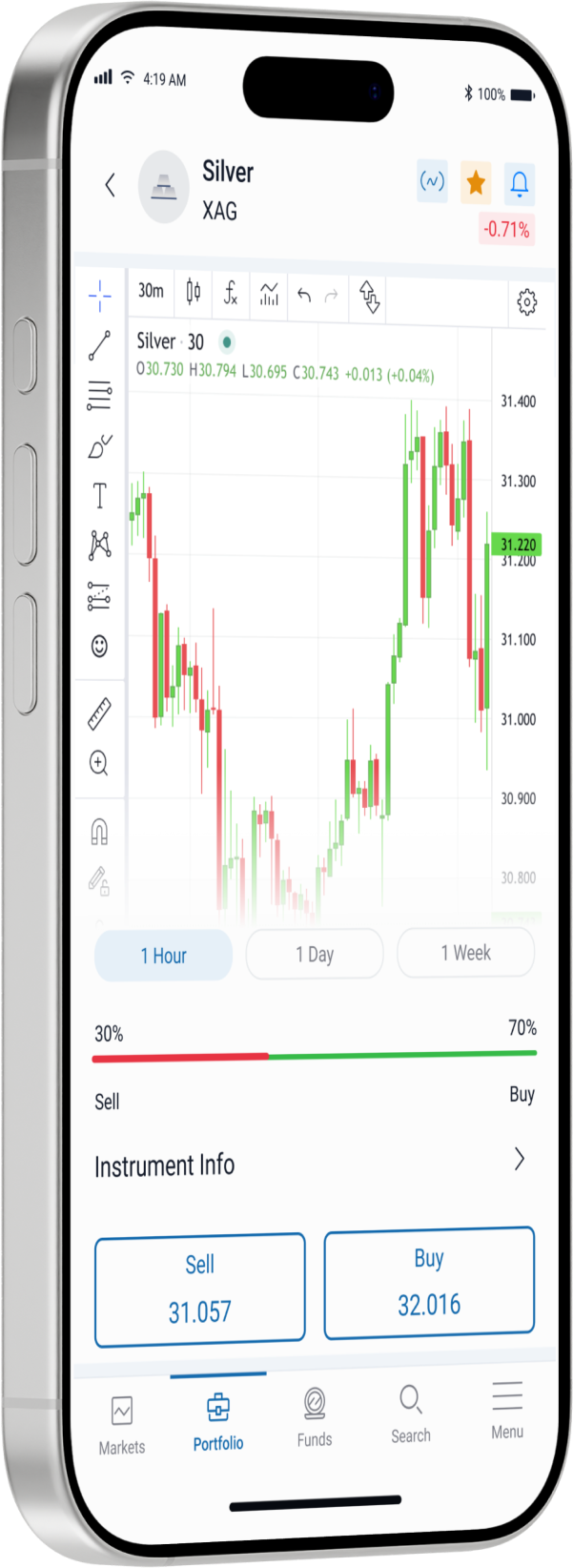

The spread is the difference between the bid price and the ask price of an instrument. The bid represents the price at which the market is willing to buy, while the ask represents the price at which it is willing to sell. The spread reflects the cost of executing a transaction immediately at current market conditions.

Spreads exist because financial markets are based on continuous matching of buyers and sellers. Market makers, liquidity providers, and exchanges facilitate this process by quoting prices that allow transactions to occur smoothly. The spread compensates for providing this liquidity and maintaining orderly pricing.

In highly liquid markets such as major currency pairs or widely traded indices, spreads tend to be narrower because large volumes of buyers and sellers participate actively. In less liquid markets, spreads may widen due to reduced participation or increased uncertainty.

Importantly, the spread is not a fixed value. It can fluctuate depending on market conditions. During periods of low liquidity or heightened volatility, spreads may temporarily expand as pricing adjusts to new information. Understanding this dynamic helps traders interpret execution costs more accurately, especially during economic releases or major news events.

How Spreads Affect Trade Entry and Exit

Because trades are executed at either the bid or ask price, the spread effectively represents the initial cost of entering a position. When a trader opens a position, it begins slightly negative relative to the midpoint price, reflecting the spread difference. For the position to move into positive territory, price must first move enough to offset that initial transaction cost.

This does not imply disadvantage. It reflects the operational reality of participating in a live market. Recognizing this mechanism encourages traders to consider trade duration, volatility, and execution timing more carefully.

Short term traders may experience the impact of spreads more frequently due to higher transaction volume. Longer term traders may be less sensitive to minor spread variations but more attentive to other cost components, such as overnight financing.

Commissions and Structured Pricing Models

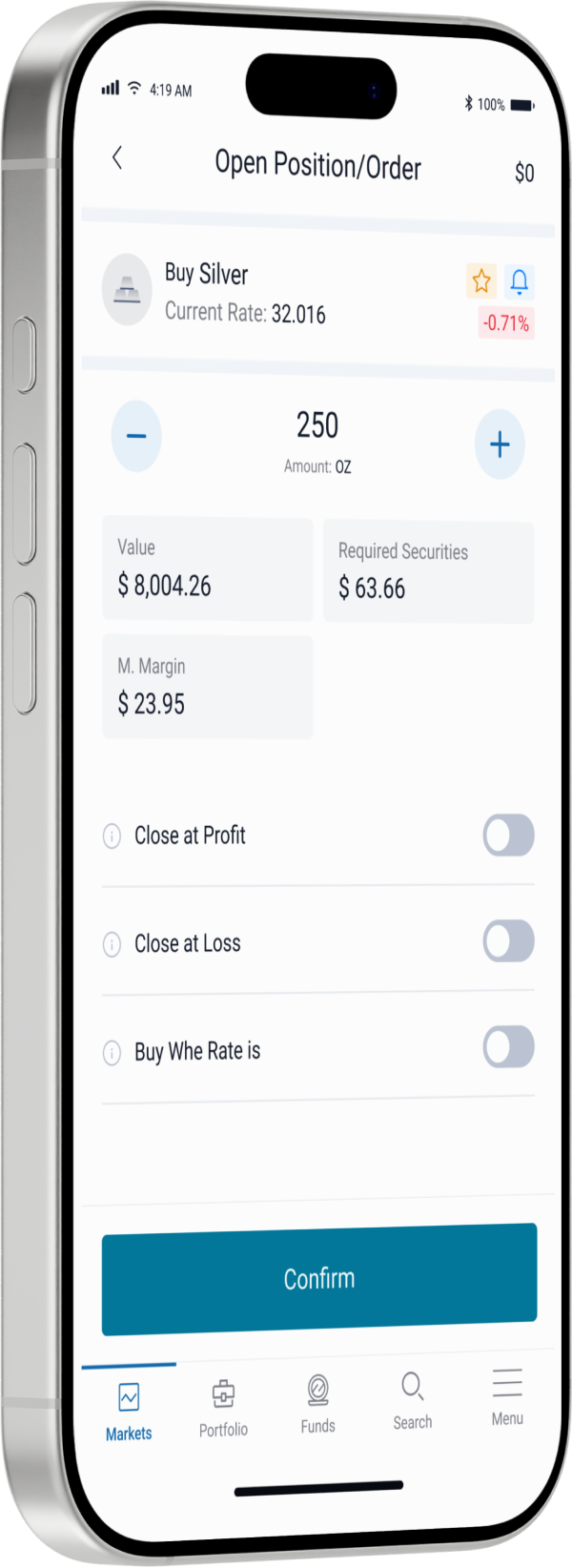

In some trading environments, commissions are charged in addition to or instead of wider spreads. A commission is a transparent fee applied per transaction, often calculated as a percentage of trade value or as a fixed cost per lot or contract.

Commission based models are common in certain asset classes, particularly equities or exchange linked products. They provide a clear and explicit pricing structure, separating execution cost from quoted pricing.

Understanding whether a trading environment incorporates cost primarily through spreads, commissions, or a combination of both is important for evaluating total transaction cost. Transparency in cost structure supports informed participation and realistic trade evaluation.

Commissions do not change market direction or probability. They represent a structural cost of accessing execution infrastructure.

Swaps and Overnight Financing

When positions are held beyond the trading day, additional costs may apply in the form of swaps or overnight financing charges. These charges reflect the cost of maintaining leveraged exposure over time and are influenced by prevailing interest rates and the characteristics of the instrument being traded.

In forex markets, swaps are typically linked to the interest rate differential between the two currencies in a pair. Holding a currency with a higher interest rate against one with a lower interest rate may result in a credit or a debit, depending on position direction. In other asset classes, financing costs may reflect borrowing expenses associated with maintaining leveraged exposure.

Overnight charges highlight the distinction between short term trading and longer holding periods. While spreads primarily affect entry and exit, swaps accumulate over time. For traders who maintain positions across multiple days or weeks, understanding how these costs accrue becomes particularly relevant.

Swaps are not penalties. They reflect the financial reality of borrowing capital to maintain leveraged exposure in global markets.

Cost Differences Across Asset Classes

Trading costs vary depending on the asset class involved. Forex markets often feature competitive spreads due to deep liquidity. Equity CFDs may include commissions alongside spreads. Commodity instruments may reflect both liquidity conditions and financing components. Digital assets may display wider spreads during periods of heightened volatility.

These differences arise from market structure, liquidity depth, regulatory environment, and instrument design. Recognizing that costs are not uniform across markets supports more informed comparison and planning.

Multi asset traders benefit from understanding how cost structures differ between instruments rather than assuming consistency across all markets.

The Relationship Between Costs and Trading Style

Different trading approaches interact with costs in different ways. Higher frequency strategies encounter spreads and commissions more frequently. Longer term strategies may experience greater sensitivity to financing charges. Active intraday participants may focus more on execution conditions during volatile periods, while swing traders may monitor cumulative swap exposure.

There is no universally optimal structure. What matters is alignment between approach and understanding. Costs should be factored into planning rather than treated as afterthoughts.

This perspective encourages realism and transparency in evaluating performance, ensuring that gross movement and net outcome are clearly distinguished.

Transparency and Platform Awareness

Modern trading platforms typically display spread information in real time and provide visibility into overnight financing rates. Reviewing this information before entering a position helps traders incorporate cost considerations into decision making.

Awareness does not eliminate cost. It integrates cost into the overall trading framework. This integration supports clearer evaluation of exposure, time horizon, and capital allocation.

Informed participation requires understanding not only how markets move, but how participation itself is structured.

Trading costs are an inherent part of accessing global financial markets. Spreads compensate liquidity provision. Commissions support execution infrastructure. Swaps reflect the cost of maintaining leveraged exposure over time. None of these elements are arbitrary. They form part of the structural foundation upon which modern trading operates.

By understanding how spreads, swaps, and commissions function, traders gain greater clarity about the mechanics of market participation. This clarity supports realistic planning, disciplined evaluation, and more transparent engagement with the markets.

In a complex financial environment, knowledge of structure is as important as knowledge of direction.

Trading CFDs involves significant risk and may not be suitable for all investors.